Understanding the EU's Omnibus Proposals: A Roadmap for the Future

ESGLOBE

8/17/20252 min read

Simplifying ESRS

Alongside communicating its first Omnibus package, the Commission has mandated EFRAG3 to amend ESRSopens in a new tab to substantially reduce the volume of disclosures – e.g. by prioritising quantitative datapoints over narrative text and clearly distinguishing between mandatory and voluntary datapoints. The concept of double materiality would remain, but the Commission intends to provide clearer instructions on applying the materiality principle. KPMG has provided feedback on EFRAG’s call for input on simplifying ESRS. The deadline for EFRAG to present the draft amendments to the Commission is 31 October 2025.

Under the proposals, the Commission no longer plans to adopt sector-specific standards.

Limiting the scope and amending the content of the EU Taxonomy

The Commission proposes making the EU Taxonomy mandatory for only a subset of large companies – i.e. those with:

more than 1,000 employees; and

a net turnover of more than EUR 450 million.

In contrast, companies wanting to claim voluntarily that their activities are taxonomy-aligned would, as a minimum, need to disclose KPIs on turnover and capital expenditure.

Additionally, the Commission is working to simplify the EU Taxonomy, including introducing a materiality threshold, simplifying the ‘Do No Significant Harm’ criteria on pollution and revising the reporting templates. These changes would apply initially in FY25 for reporting in 2026. Read KPMG EMA DPP's comment letter on the EU Taxonomy consultation.

What other key changes are proposed?

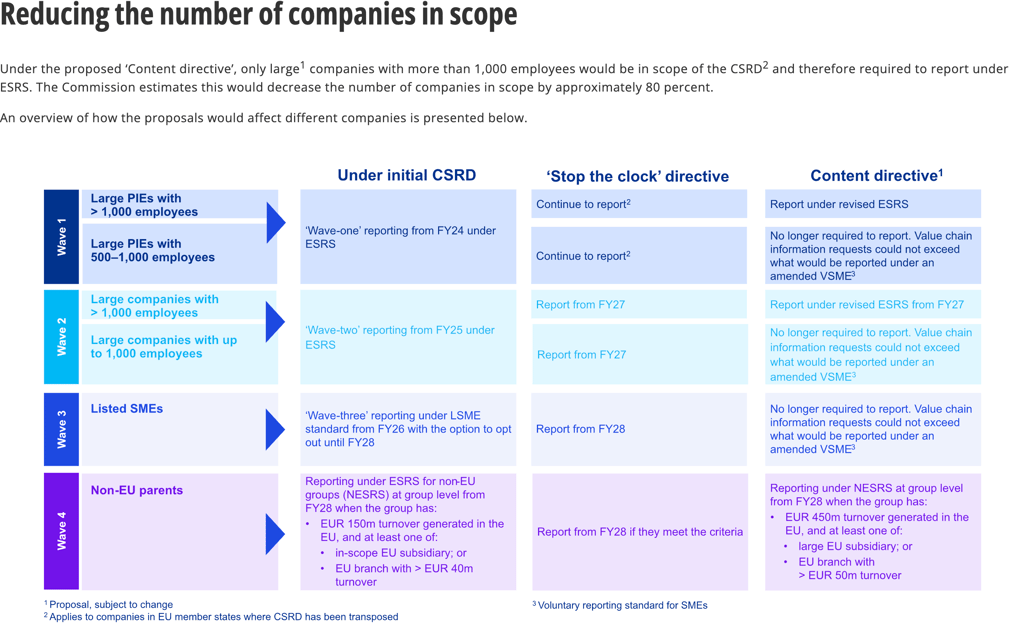

The Commission proposes changing the CSRD to protect smaller companies (up to 1,000 employees) by limiting the ‘trickle-down effect’. Requests for value chain information could not exceed what would be reported under an amended voluntary reporting standard for SMEs (VSME).

The CSRD would still require limited assurance, but the Commission no longer intends to move to reasonable assurance. In addition, the deadline for a European limited assurance standard would be removed.

On the CSDDD4, the Commission proposes significant changes to reduce the compliance burden on companies. The proposals include delaying initial application by one year, reducing the number of business partners and stakeholders to consider, and less frequent assessments.

How can companies prepare for the changes?

With the release of the Commission’s first Omnibus package, now is a good time for companies to identify any ‘no-regret moves’ that they can focus on, such as:

revisiting CSRD scoping to understand how the proposed thresholds might influence reporting;

reprioritising efforts and focusing on strategic actions that go beyond compliance, for example:

transition planning;

materiality assessment; and

a focus on the data that is relied on for strategic decision making.

continuing dialogue with stakeholders around policies, actions and targets across material topics and clarifying sustainability-related messaging; and

with reporting under IFRS® Sustainability Disclosure Standards from the ISSB5 on the horizon in various major jurisdictions outside the EU, considering moving forward on climate, particularly preparing Scope 1, 2 and 3 greenhouse gas emissions inventory and identifying and mitigating climate-related risks.